Toggle navigation

Home

About Us

Latest News

Clients

Information Pages

What is Financial Planning?

Our Financial Planning Process

Savings & Investment Strategies

Death & Disability Insurance

Superannuation & Retirement

Latest News from Newealth

Share this archive

Latest News Posts

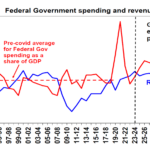

Market Metrics: Global Listed Companies

23 June, 2025

American Exceptionalism: R&D Investment

19 June, 2025

Friday Tidbit

6 June, 2025

AFR Rich List: Billionaire Debuts

28 May, 2025

Up to a 50% guaranteed return

8 May, 2025

Warren Buffett, The Oracle of Omaha

6 May, 2025

Market Metrics: Inflation

1 May, 2025

Things that sparkle

31 March, 2025

2025 Budget

26 March, 2025

Recession ???

24 March, 2025

Archives

June 2025

(3)

May 2025

(4)

March 2025

(6)

Top